Tax Cuts and Jobs Act

Tax Act Overview The Tax Cuts and Jobs Act of 2017, which we will simply call the “Tax Act”, is not retroactive except for a very few unique expensing provisions, so for nearly everyone, your upcoming income tax filing due this spring for the 2017 tax year filing will NOT be effected. However, the changes…

3 Ways to Prepare Now for Taxes

It may seem early, but the start of a new year is an ideal time to get your ducks in a row when it comes to tax preparation. Use the following tips to get some work done now and avoid the panic of procrastination. Revisit Your Usual Routine The bulk of tax prep comes down…

Where to Retire

If you’re like most of our clients, you’ve thought long and hard about the financial aspects of your retirement. You’ve likely worked hard and saved diligently. But, retirement for each person is different. Perhaps you plan on a working retirement with a new job and less stress, focused on what you love. Or, perhaps you…

Alternative Minimum Tax (AMT)

Well, it’s almost April 18th (the tax deadline is extended three days this year). If you’re like most people waiting until the last minute to file, you likely anticipate owing taxes instead of receiving a refund. And, if you owe tax, you may have higher than average income, which means at some point, you could…

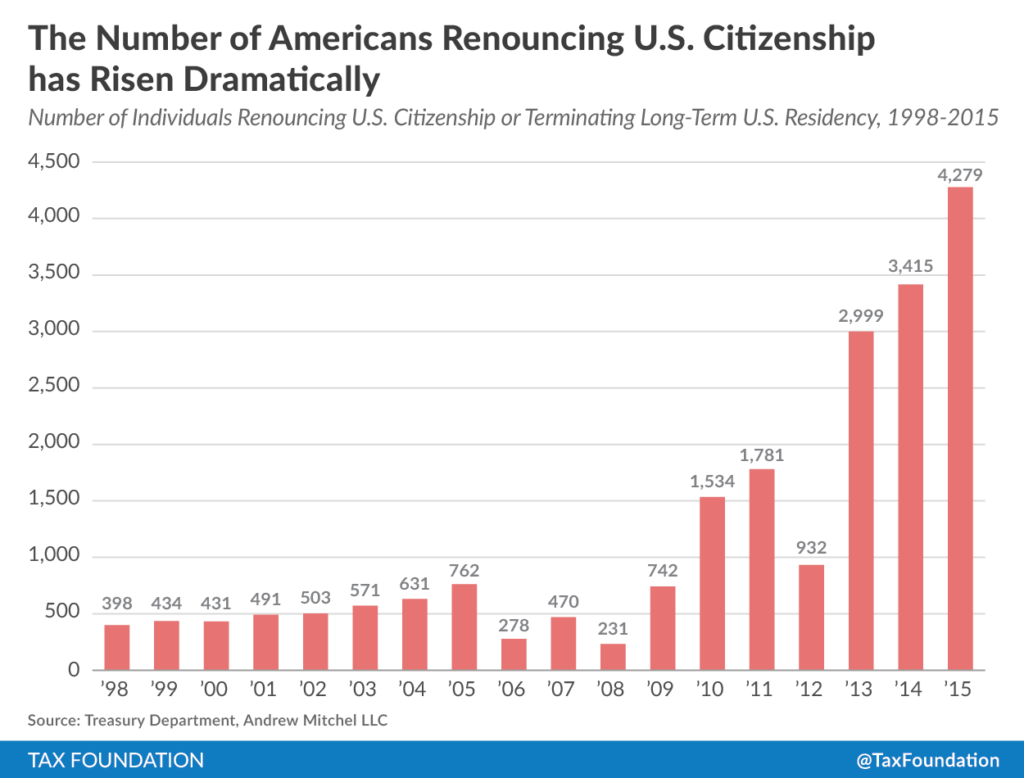

Record Numbers Renouncing U.S. Citizenship

According to the Treasury Department, 4,279 people renounced their American citizenship in 2015. This is up 864 from the previous high of 3,415 in 2014. From 2013 to 2015, 10,693 citizens have renounced their citizenship, which is more than the 10,189 renouncements in the previous 15 years from 1998 to 2012. So why are so…

The IRS Phone Scam

As we all know, there are many scams taking place every day in our modern world, but one of the fastest growing is an IRS scam. So, with tax season fast approaching, we wanted to make you aware of the latest tactic by scammers to use you and the IRS. In short the scam involves…

We hope you find our financial and economic insights helpful, but if you need more in-depth or personal guidance just Contact Us. We'd be honored to assist you with nearly any Service that effects you or your organization's finances!

recent comments